What Is SOX 404 Compliance and How Can You Achieve It?

What is SOX 404 compliance and how can you achieve it? One surefire way to be in compliance is through the COSO framework. Learn more here.

Blog Post

8 minute read

Nov 20, 2023

Section 404 of the Sarbanes-Oxley Act (SOX) requires any and all publicly traded companies to establish, test, and maintain internal processes that govern financial reporting. Additionally, SOX 404 compliance is also a necessity for whole-owned subsidiaries and publicly-traded foreign companies that do business in the US.

The Sarbanes-Oxley Act was created after a number of high-profile corporate scandals during the early 2000s and was established to mitigate fraud and increase transparency through consistent and accurate financial reporting.

There are a number of sections within SOX’s 11 titles, but some will be more pertinent to businesses because of their scope and cost—specifically SOX 404, which concerns the assessment of internal controls in financial reporting.

SOX 404 compliance can be very costly, but through modern technology and document management, many previously manual processes can be automated, reducing risk and cost.

In this blog post, we’re going to take a look at SOX 404, including what it requires and how organizations can comply.

Complying with industry regulations on data privacy and security is only one branch of a comprehensive cybersecurity strategy. Learn what else goes into a strong cybersecurity posture in Impact’s blog, What is Layered Security in Cybersecurity?

What Is SOX Section 404?

Section 404 of the Sarbanes-Oxley Act is the most costly and complex aspect of SOX compliance. That said, it’s a vital section for businesses to address as it concerns annual financial reporting.

Section 404 requires that annual reports include the company’s own assessment of their internal controls on financial reporting, as well as an assessment conducted by a third-party auditor.

The third-party audit is required to demonstrate the reliability and accuracy of a company’s internal controls and acts as a way to ensure the integrity of financial reports.

Under Section 404, SEC registrants will be required to include with their annual filing:

A statement of management’s responsibility for establishing and maintaining adequate internal control over financial reporting

A statement identifying the framework used by management to evaluate the effectiveness of internal control

Management’s assessment of the effectiveness of internal control as of the end of the company’s most recent fiscal year end

A statement that the company’s external auditor has issued an attestation report on management’s assessment

What are Internal Controls?

While Section 404 of the Sarbanes-Oxley Act requires that publicly traded companies to establish internal controls around financial reporting, the act doesn’t offer specific processes or procedures to instill.

This has led to a variety of solutions that different organizations use in order to standardize and regulate financial reporting practices internally.

Fortunately, there are existing frameworks, notably the COSO Internal Control Framework, developed as a joint initiative between five organizations: Institute of Internal Auditors (IIA), American Institute of Certified Public Accountants (AICPA), Financial Executives International (FEI), The Association of Accountants and Financial Professionals in Business (IMA), and American Accounting Association (AAA).

Companies looking to comply with the Sarbanes-Oxley Act Section 404 can look to the COSO framework of financial controls and reporting practices that comply with SOX 404.

The COSO Framework

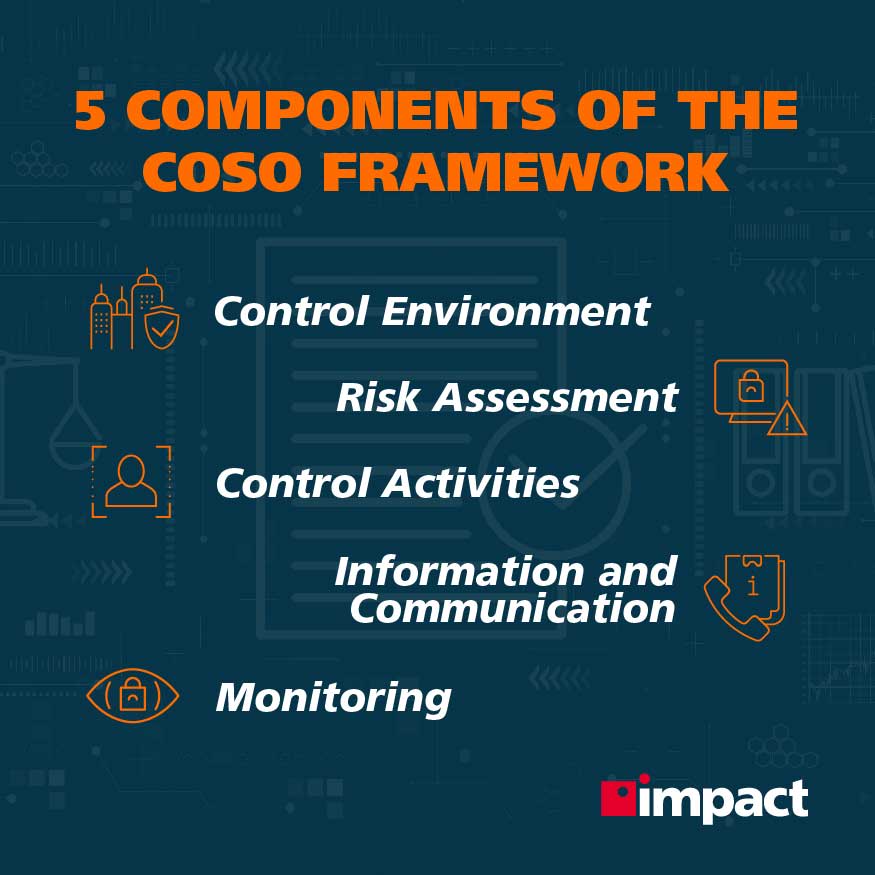

The COSO framework contains 17 principles within five subsections, known as components, that should be followed in order to demonstrate to a third-party auditor that the company is in compliance with SOX 404 cybersecurity requirements.

Control Environment

The control environment lays out the set of standards and processes that are the foundation for carrying The first component of the COSO Framework is the control environment. The control environment lays out the set of standard processes and procedures that create the foundation for transparent, regulated internal financial reporting.

Establishing an effective strategy to regulate internal reporting is predicated on the control environment, and should be driven by strategic goals, such as:

Providing reliable financial reporting to internal and external stakeholders

Operating with transparency

Operating the business efficiently and effectively

Complying with all applicable laws and regulations

Safeguarding assets and sensitive information

The control environment is dictated by organizational leadership and should be reinforced by things like the mission and vision statements, documented policies, and other top-down initiatives that establish a culture of transparency and ethical operations.

By establishing a strong control environment as a part of the company culture, your organization also:

Demonstrates commitment to integrity and ethical values

Ensures that the board exercises oversight responsibly

Establishes structures, reporting lines, authorities, and responsibilities

Demonstrates commitment to a competent and ethical workforce

Holds people accountable

The Risk Assessment for SOX

A risk assessment for SOX 404 compliance is crucial for determining what a company’s risk factors are and how they can be mitigated.

In this case, “risk” is defined as the probability that an event will occur that disrupts business objectives. A risk assessment requires top management to scrutinize their internal control environment and make any necessary adjustments to internal reporting processes.

By conducting a risk assessment, organizations will be able to better map out compliance strategies and the path they need to tread to reach their goals. The risk assessment also helps leaders:

Specify appropriate objectives

Identify and analyze risks

Evaluate fraud risks

Identify and analyze changes that could significantly affect internal controls

Control Activities

Control activities regard the actions taken that can help mitigate risks identified during the risk assessment phase. These activities may be preventive or detective and can be performed at all levels within an organization.

Establishing processes and procedures based on the risk assessment conducted is crucial for organizations who need to improve their compliance posture and internal reporting methods.

This phase of the COSO framework is when your company will:

Select and develop control activities that mitigate risks

Select and develop technology controls

Deploy control activities through policies and procedures

Information & Communications

Information and communications flowing up, down, and across organizations is shared effectively and efficiently.

Information systems and repositories must provide the appropriate stakeholders with information that is relevant to their established objectives in a timely and succinct manner. Not only that, but reports need to be accurate and verifiable.

The main purpose of SOX 404 compliance is to deter fraudulent reporting both internally and externally.

As such, the role of communications in this framework is to:

Use relevant, quality information to support the internal control function

Communicate internal control information internally

Communicate internal control information externally

Monitoring

Ongoing evaluations of internal controls should be adopted by the organization in order to ensure that the internal control functions established are operating correctly and resulting in both accurate and transparent reports.

When deficiencies are found, these should be evaluated and communicated in a timely manner to senior management and the board of directors (if necessary) so that they can be addressed quickly and your organization can return to compliance.

By monitoring your reporting processes on an on-going basis, your company can effectively:

Discover and identify problem issues within the established processes and procedures

Communicate internal control deficiencies

Address any gaps discovered by on-going audits

Why Should You Establish the COSO Framework In Your Business?

If an organization fails to implement the controls of the COSO framework or other SOX 404 compliance guidelines, they may very well be in violation of compliance requirements mandated under federal law for financial reporting.

Auditors will judge a company’s internal control capabilities against the COSO framework, so it’s best for companies to hold themselves to that standard in order to abide by SOX.

How to Implement the COSO Framework

COSO implementation involves assessing where an organization currently is among its five subsections and understanding what’s needed in order to get up to standard operating compliance.

This will comprise a SOX audit, which should incorporate the COSO framework and an assessment of the 17 principles referred to earlier, typically in three distinct stages:

1. Planning and Scope

2. Execution

3. Analysis and Reporting

1. Planning and Scope

Implementation starts at the beginning: key stakeholders will be engaged and the cybersecurity auditors will designate the correct stakeholders for each of the principles.

For example, c-suite executives will be engaged for many of the Control Environment activities, while IT personnel may be engaged for technology policy and procedure principles, and a compliance may be engaged as the key stakeholder for monitoring principles.

Auditors will need to have a complete picture of where all business data is stored, including in third-party applications operating under the company network.

2. Execution

The auditors will conduct penetration testing and vulnerability scanning in order to clearly establish where the business stands with its current model within the COSO framework.

3. Analysis and Reporting

These results will then be reported to the key stakeholders and recommendations will be made to help get the business in compliance with the COSO framework, at which point the organization can be confident they are SOX 404 compliant.

Wrapping Up on SOX 404 Compliance

SOX 404 compliance is a necessary but frankly rather complex form of compliance for publicly-traded companies.

The requirements of SOX 404 mean adherence to the COSO framework. Its 17 principles offer a solid foundation and means for an organization to be SOX 404 compliant, and it’s a good idea for companies to follow this standard to get their internal controls up to standard.

To implement the COSO framework, businesses should consider hiring a managed security service provider to audit their systems and provide recommendations on which solutions, policies, and procedures should be adopted to get in compliance.

Compliance regulations help your organization implement security practices, processes, and policies that better protect you and your employee’s information, but this is just one piece of the puzzle. Learn what other tactics play a critical role in your cybersecurity posture in Impact’s blog, What is Layered Security in Cybersecurity?